全部商品分类

| 联系编辑 | |

|---|---|

| 标题: | |

| 内容: | |

| 联系方式: | |

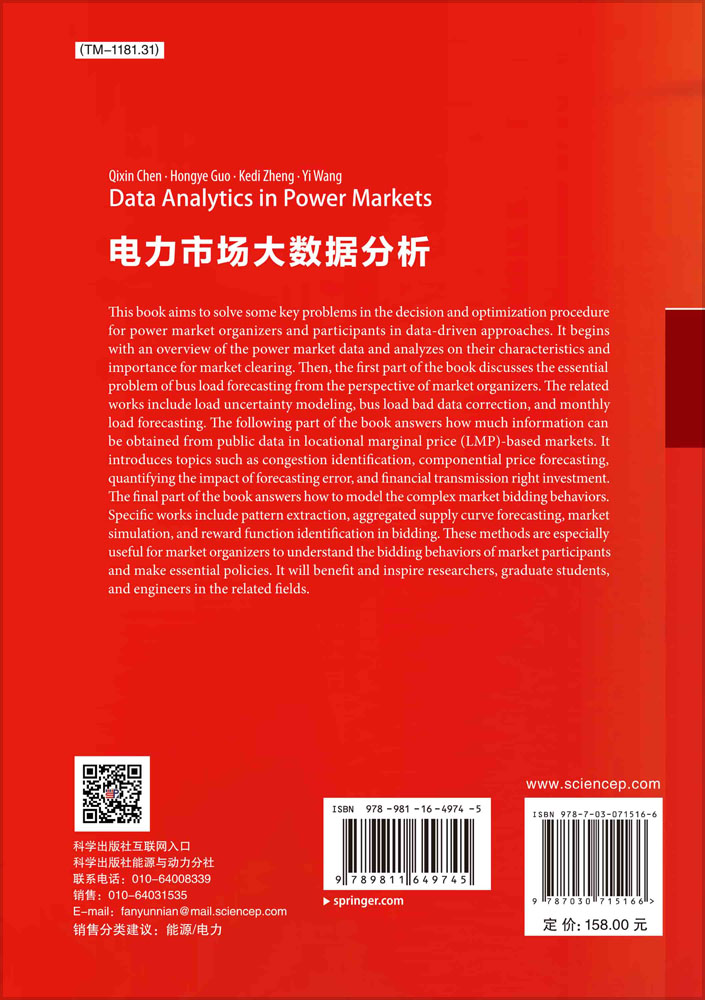

本书以电力市场领域近年来的研究工作成果为基础,力图系统性地介绍电力市场中的数据价值挖掘方法以支撑市场组织者和市场参与者的决策问题。本书围绕电力市场中的公开数据和机器学习方法理论与应用展开,结合电力市场规则和物理特征,期望解决市场规则解析和数据结构化两大核心难点,并从负荷与电价预测、报价行为解析、金融衍生品投机等方面,构建了电力市场数据分析理论和技术方法体系。

全书共13章,第1章介绍了世界各地的电力市场数据概况。除第1章外,剩余内容分为三部分。第一部分为负荷建模与预测,包括了基于智能电表数据的负荷预测方法等。第二部分为电价建模与预测,包括了节点电价数据的子空间特性建模等。第三部分为市场投标行为分析,包括了机组投标行为的特征提取方法等。

样章试读

- 暂时还没有任何用户评论

全部咨询(共0条问答)

- 暂时还没有任何用户咨询内容

|

中国科技出版传媒股份有限公司 版权所有 本平台为互联网非涉密平台,严禁处理、传输国家秘密。 京ICP备14028887号-5 京ICP证150976号

北京东黄城根北街16号 邮编:100717 Email:webmaster@mail.sciencep.com |

京公网安备 11010102004214号

京公网安备 11010102004214号