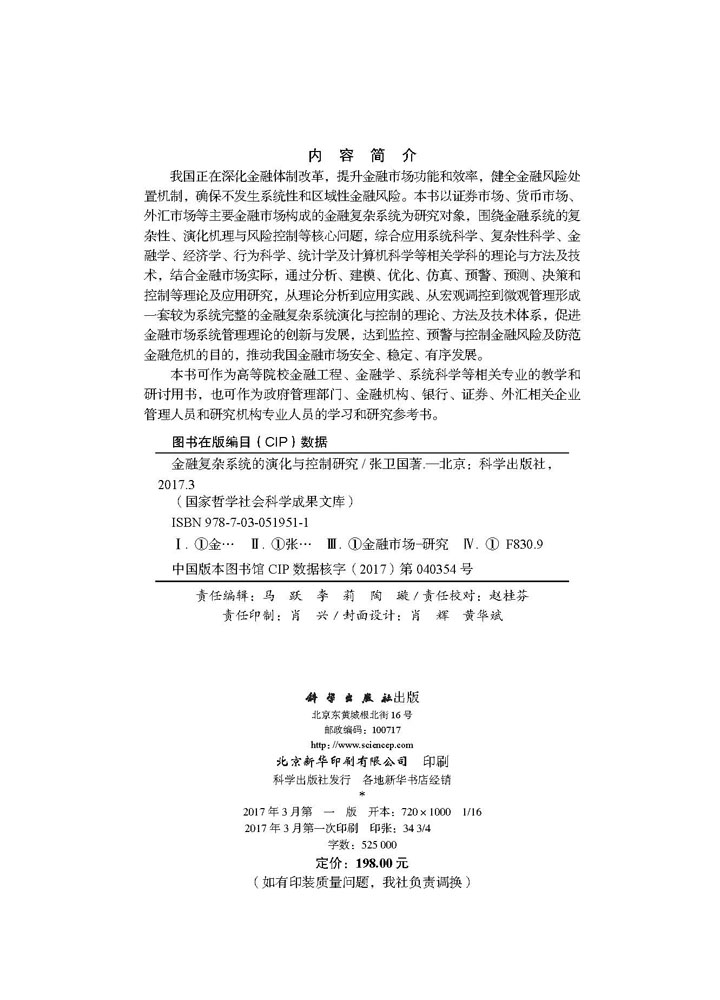

我国正在深化金融体制改革,提升金融市场功能和效率,健全金融风险处置机制,确保不发生系统性和区域性金融风险。本书以证券市场、货币市场、外汇市场等主要金融市场构成的金融复杂系统为研究对象,围绕金融系统的复杂性、演化机理与风险控制等核心问题,综合应用系统科学、复杂性科学、金融学、经济学、行为科学、统计学及计算机科学等相关学科的理论与方法及技术,结合金融市场实际,通过分析、建模、优化、仿真、预警、预测、决策和控制等理论及应用研究,从理论分析到应用实践、从宏观调控到微观管理形成一套较为系统完整的金融复杂系统演化与控制的理论、方法及技术体系,促进金融市场系统管理理论的创新与发展,达到监控、预警与控制金融风险及防范金融危机的目的,推动我国金融市场安全、稳定、有序发展。

样章试读

目录

- 目录

导论 (1)

第一部分 金融市场的相互作用及关系研究

第1章 中国金融市场发展现状 (15)

1.1 引言 (15)

1.2 主要金融市场概念界定 (16)

1.3 中国主要金融市场发展现状 (19)

1.4 货币市场、股票市场及外汇市场关系研究 (25)

1.5 本章小结 (28)

第2章 中国主要金融市场发展协调性评价研究 (31)

2.1 引言 (31)

2.2 金融市场发展协调性内涵及理论基础 (31)

2.3 金融市场发展协调性评价指标体系 (33)

2.4 金融市场发展协调性实证分析 (41)

2.5 本章小结 (63)

第3章 多个金融市场波动溢出模型及实证研究 (66)

3.1 引言 (66)

3.2 多元波动率模型 (68)

3.3 基于独立成分分析的IC-EGARCH模型 (69)

3.4 中国多个金融市场波动溢出实证分析 (72)

3.5 本章小结 (76)

第4章 多国和地区股票市场间的暴跌交互作用研究 (79)

4.1 引言 (79)

4.2 Hawkes过程建模 (80)

4.3 多国和地区股票市场实证分析 (82)

4.4 本章小结 (90)

第二部分 金融复杂系统的特征及非线性系统分析

第5章 金融市场系统复杂性特征及结构 (97)

5.1 引言 (97)

5.2 金融市场系统复杂性的整体特征 (100)

5.3 金融市场系统复杂性的时空演变结构 (104)

5.4 本章小结 (105)

第6章 金融市场系统复杂性的演化机理研究 (108)

6.1 引言 (108)

6.2 动态演化的三体“束缚”模型 (109)

6.3 基于朗之万方程的非线性动力学模型 (112)

6.4 适应性演变的反馈模式 (114)

6.5 应用分析:股票市场中的泡沫现象 (117)

6.6 本章小结 (119)

第7章 基于金融政策目标的非线性演化模型与实证分析 (122)

7.1 引言 (122)

7.2 主要金融市场“束缚”结构下非线性演化模型 (125)

7.3 金融政策目标指标的构建 (125)

7.4 金融政策目标非线性演化的实证分析 (127)

7.5 本章小结 (133)

第8章 基于金融市场指标的非线性演化模型与实证分析 (136)

8.1 引言 (136)

8.2 市场指标选取 (138)

8.3 因果关系检验 (139)

8.4 三个市场综合指数的建立 (144)

8.5 非线性演化模型 (145)

8.6 实证检验与结果分析 (148)

8.7 本章小结 (152)

第三部分 金融市场的分形分析及资产定价研究

第9章 金融市场多重分形特征研究 (157)

9.1 引言 (157)

9.2 分形与多重分形理论 (159)

9.3 中国股票市场的多重分形特征研究 (163)

9.4 马尔可夫转换多重分形模型及波动率预测 (171)

9.5 本章小结 (177)

第10章 金融市场波动率长记忆性及参数估计方法 (179)

10.1 引言 (179)

10.2 随机波动率 (181)

10.3 金融时间序列的长记忆性 (183)

10.4 长记忆随机波动率的参数估计方法 (184)

10.5 连续时间框架下的赫斯特指数估计 (198)

10.6 中国股票市场长记忆性实证研究 (203)

10.7 本章小结 (204)

第11章 分形环境下股本权证定价模型研究 (208)

11.1 引言 (208)

11.2 分形环境下股本权证的定价模型 (210)

11.3 公司股票价格行为模式 (211)

11.4 定价模型的性质 (215)

11.5 应用研究 (218)

11.6 本章小结 (219)

第12章 分数Vasicek过程下零息票债券的定价模型及参数估计 (222)

12.1 引言 (222)

12.2 分数Vasicek随机利率模型及其零息票债券定价模型 (224)

12.3 机器学习下的参数估计方法 (226)

12.4 本章小结 (229)

第13章 次分数布朗运动下带交易费用的备兑权证定价 (231)

13.1 引言 (231)

13.2 备兑权证定价模型 (232)

13.3 参数估计 (237)

13.4 实证分析 (238)

13.5 本章小结 (240)

第四部分 金融复杂系统的人工智能技术

第14章 几何亚式期权的模糊定价方法及应用 (247)

14.1 引言 (247)

14.2 几何亚式期权的模糊定价模型 (249)

14.3 算法分析与数值算例 (256)

14.4 实证分析 (261)

14.5 本章小结 (263)

第15章 融合ICA的BP网络多种人民币汇率预测方法 (265)

15.1 引言 (265)

15.2 IC-BP网络预测方法 (266)

15.3 多种人民币汇率预测应用分析 (269)

15.4 本章小结 (275)

第16章 DE-ELM预测模型及股指预测应用 (277)

16.1 引言 (277)

16.2 模型及算法介绍 (279)

16.3 双层DE-ELM预测模型 (282)

16.4 股指预测实证分析 (286)

16.5 本章小结 (292)

第17章 基于模型预测控制和TVP-VAR模型的货币政策仿真研究 (294)

17.1 引言 (294)

17.2 货币政策的目标函数 (297)

17.3 时变系数的向量自回归模型 (299)

17.4 基于随机模型预测控制的利率调控仿真 (304)

17.5 本章小结 (310)

第五部分 金融复杂系统的计算机模拟实验与行为研究

第18章 基于ACP方法的金融复杂性平行系统研究 (315)

18.1 引言 (315)

18.2 相关理论 (316)

18.3 基于ACP方法的金融复杂性平行系统构建 (319)

18.4 银行利率和股票交易印花税对股价影响的仿真实验 (325)

18.5 本章小结 (327)

第19章 基于投资者情绪的资产定价模型 (330)

19.1 引言 (330)

19.2 高阶期望理性资产定价模型 (332)

19.3 高阶期望情绪资产定价模型 (335)

19.4 异质投资者情绪资产定价模型 (340)

19.5 本章小结 (344)

第20章 股指期货情绪与收益的联动性及期限结构研究 (346)

20.1 引言 (346)

20.2 市场情绪的构建 (347)

20.3 股指期货情绪期限结构 (351)

20.4 多市场情绪与股指期货收益的联动性研究 (354)

20.5 本章小结 (360)

第21章 基于EEMD的投资者情绪与股指波动的关系研究 (363)

21.1 引言 (363)

21.2 集成经验模态分解方法 (366)

21.3 投资者情绪指数的测度 (368)

21.4 实证结果及分析 (370)

21.5 本章小结 (379)

第六部分 金融复杂系统的预警机制研究

第22章 中国金融市场风险指数与风险程度测量 (385)

22.1 引言 (385)

22.2 主要金融市场风险指数 (387)

22.3 主要金融市场风险程度测量 (392)

22.4 本章小结 (399)

第23章 中国金融市场先行指标与风险传染路径 (401)

23.1 引言 (401)

23.2 金融市场先行指标选择 (404)

23.3 金融风险传染路径分析 (408)

23.4 本章小结 (410)

第24章 中国金融风险预警与有效性检验 (412)

24.1 引言 (412)

24.2 金融风险预警指标及判断标准 (416)

24.3 发达国家的金融风险预警体系 (419)

24.4 中国金融风险预警现状 (422)

24.5 中国金融风险预警指数构建与有效性检验 (423)

24.6 本章小结 (427)

第七部分 金融复杂系统的风险控制与对策研究

第25章 基于多元分析的人民币汇率波动率预测及应用 (431)

25.1 引言 (431)

25.2 多元波动率模型 (432)

25.3 模型的检验 (437)

25.4 多元波动率的预测 (438)

25.5 人民币汇率波动率预测的实证分析 (439)

25.6 本章小结 (444)

第26章 基于股指期货的风险管理方法及应用 (447)

26.1 引言 (447)

26.2 股指期货展期套期保值模型 (449)

26.3 最优展期套期保值策略 (454)

26.4 考虑交易成本的展期套期保值模型及最优策略 (460)

26.5 本章小结 (466)

第27章 模糊环境下投资组合优化方法及应用 (469)

27.1 引言 (469)

27.2 基本理论 (472)

27.3 具有最小交易手数的多期投资组合选择模型 (474)

27.4 求解算法 (480)

27.5 实证分析 (484)

27.6 本章小结 (487)

第28章 基于随机模型预测控制的欧式期权动态对冲 (492)

28.1 引言 (492)

28.2 构建资产价格变动模型 (494)

28.3 基于情景模拟的随机模型预测控制 (498)

28.4 仿真分析 (501)

28.5 本章小结 (505)

第29章 对策研究 (508)

29.1 在复杂性思维下构建中国金融系统的宏观审慎体系 (508)

29.2 加快建设中国金融市场系统性风险防范体系的思路 (512)

29.3 中国资本项目开放和汇率制度改革及人民币国际化协调对策(516)

29.4 中国货币市场与股票市场协调发展的问题及对策 (520)

索引(527)

后记(529)

CONTENTS

Introduction/1

Part 1 Research on Interactions and Relationships of Financial Markets

Chapter 1 Current Situation of Development in China ’ s Financial markets/15

1.1 Introduction/15

1.2 Definition of Major Financial Market/16

1.3 Status of China’s Major Financial Markets/19

1.4 Relationships Among Monetary,Securities and Foreign Exchange Markets/25

1.5 Conclusion/28

Chapter 2 Coordination Evaluation Indicator System of Major Financial Markets in China/31

2.1 Introduction/31

2.2 Financial Markets’Coordination Connotation of Development and Theoretical Basis/31

2.3 Financial Markets’Coordination Evaluation Indicator System/33

2.4 Empirical Analysis on Coordination of Development of Major Financial Markets/41

2.5 Conclusion/63

Chapter 3 Volatility Spillover Effect and Empirical Study on multi-financial Markets/66

3.1 Introduction/66

3.2 Multivariate Volatility Models/68

3.3 IC-EGARCH Models Based on Independent Component Analysis/69

3.4 Empirical Study of Volatility Spillover Effect on China’s Multifinancial Markets/72

3.5 Conclusion/76

Chapter 4 Interaction of Crash in Stock Markets of Many Countries and Regions/79

4.1 Introduction/79

4.2 Hawkes Process Model/80

4.3 Empirical Study of Many Countries and Regions/82

4.4 Conclusion/90

Part 2 Characteristics and Nonlinear Systemic Analysis of Complex Financial Systems

Chapter 5 Characteristics and Structure of Complex Financial Systems/97

5.1 Introduction/97

5.2 Systemic Characteristics of Complexity in Financial Markets/100

5.3 Spatiotemporal Evolution Structure of Systemic Complexity in Financial Markets/104

5.4 Conclusion/105

Chapter 6 Evolution Mechanisms of Systemic Complexity in Financial Markets/108

6.1 Introduction/108

6.2 Dynamic Three-body“Bondage”Model/109

6.3 Nonlinear Dynamical Model Based on Langevin Equation/112

6.4 Feedback Model with Adaptive Evolution/114

6.5 Application:Bubbles in the Stock Market/117

6.6 Conclusion/119

Chapter 7 Nonlinear Evolution Model and Empirical Analysis Based on Financial Policy Goals/122

7.1 Introduction/122

7.2 Nonlinear Evolution Model with“Bondage”Structure in Major Financial Markets/125。

7.3 Construction of Financial Policy Goal Indicators/125

7.4 Empirical Analysis on the Nonlinear Evolution of Financial Policy Goals /127

7.5 Conclusion/133

Chapter 8 Nonlinear Evolution Model and Empirical Analysis Based on Financial Market Indicators/136

8.1 Introduction/136

8.2 Selection of Market Indicators/138

8.3 Causality Test/139

8.4 Construction of Three Comprehensive Market Indicators/144

8.5 Nonlinear Evolution Model/145

8.6 Empirical Tests and Analysis/148

8.7 Conclusion/152

Part 3 Research on Fractal Analysis and Asset Pricing of Financial Market

Chapter 9 Research on Multifractal Characteristics of Financial Market/157

9.1 Introduction/157

9.2 Fractal and Multifractal Theory/159

9.3 Multifractal Analysis of China’s Stock Market/163

9.4 Markov Switching Multifractal Model and Volatility Forecasting/171

9.5 Conclusion/177

Chapter 10 Long-memory Stochastic Volatility and Parameter Estimation in Financial Market/179

10.1 Introduction/179

10.2 Stochastic Volatility/181

10.3 Long Memory Property of Financial Time Series/183

10.4 Parameter Estimation of Long-memory Stochastic Volatility/184

10.5 Parameter Estimation for Hurst Index in the Framework of Continuous Time/198

10.6 Empirical Study of Long-memory in China’s Stock Market/203

10.7 Conclusion/204

Chapter 11 Pricing Model for Equity Warrants in a Fractional Environment/208

11.1 Introduction/208

11.2 Pricing Model for Equity Warrants in a Fractional Environment/210

11.3 Patterns of Change in Stock Price/211

11.4 Properties of Pricing Model/215

11.5 Application Study/218

11.6 Conclusion /219

Chapter 12 Pricing Model of Zero-coupon Bond and Parameter Estimation Under the Fractional Vasicek Process/222

12.1 Introduction/222

12.2 Stochastic Interest Rate Model of Fractional Vasicek Process and Its Pricing Model for Zero-coupon Bond/224

12.3 Parameter Estimation Based on Machine Learning/226

12.4 Conclusion/229

Chapter 13 Pricing Covered Warrants in a Sub-fractional Brownian Motion with Transaction Costs/231

13.1 Introduction/231

13.2 Pricing Model for Covered Warrants/232

13.3 Parameter Estimation/237

13.4 Empirical Analysis/238

13.5 Conclusion/240

Part 4 Artificial Intelligence Technology of Complex Financial Systems

Chapter 14 Fuzzy Pricing Method and Application of Geometric Asian Options/247

14.1 Introduction/247

14.2 Fuzzy Pricing Model of Geometric Asian Options/249

14.3 Algorithm Analysis and Numerical Examples/256

14.4 Empirical Analysis/261

14.5 Conclusion/263

Chapter 15 BP Neural Networks Method Combining with ICA for Forecasting Multivariate RMB Exchange Rate/265

15.1 Introduction/265

15.2 IC-BP Neural Networks Method/266

15.3 Application Analysis of Forecasting Multivariate RMB Exchange Rate/269

15.4 Conclusion/275

Chapter 16 DE-ELM Forecasting Model and Medium-short Term Prediction of Stock Index/277

16.1 Introduction/277

16.2 Model and Algorithm/279

16.3 Double-layer DE-ELM Forecasting Model/282

16.4 Empirical Analysis of Stock Index Prediction/286

16.5 Conclusion/292

Chapter 17 Research on the Monetary Policy Simulation Based on Model Predictive Control and TVP-VAR Model/294

17.1 Introduction/294

17.2 Objective Function of Monetary Policy/297

17.3 Time-varying Parameter VAR Model/299

17.4 Interest Rate Control Simulation Based on Stochastic Model Predictive Control/304

17.5 Conclusion/310

Part 5 Simulations and Behavioral Analysis of Complex Financial Systems

Chapter 18 Research on the Parallel Complex Financial Systems Based on the ACP Method/315

18.1 Introduction/315

18.2 Theories/316

18.3 Construction of the Parallel Complex Financial Systems Based on the ACP Method/319

18.4 Simulation of Interest Rates at Bank and Stamp Duty on Stock Price/325

18.5 Conclusion/327

Chapter 19 Sentiment Asset Pricing Model with Information/330

19.1 Introduction/330

19.2 Rational Asset Pricing Model with Higher Order Expectations/332

19.3 Sentiment Asset Pricing Model with Higher Order Expectations/335

19.4 Sentiment Asset Pricing Model with Heterogeneous Order Expectations /340

19.5 Conclusion/344

Chapter 20 Research on the Linkage Between the Sentiment in Stock Index Futures and Return with the Term Structure/346

20.1 Introduction/346

20.2 Construction of Market Sentiment/347

20.3 Term Structure of Sentiment in Stock Index Futures/351

20.4 Co-movement Between Multimarket Sentiment and Stock Index Futures Returns/354

20.5 Conclusion/360

Chapter 21 Study on the Relationships Between Investor Sentiment and Stock Index Volatility Based on EEMD/363

21.1 Introduction/363

21.2 Ensemble Empirical Mode Decomposition Method/366

21.3 Measure of Investor Sentiment Index/368

21.4 Empirical Results and Analysis/370

21.5 Conclusion/379

Part 6 Research on the Early Warning Mechanism of Complex Financial Systems

Chapter 22 Risk Index and Risk Measurement of China’s Financial Markets/385

22.1 Introduction/385

22.2 Risk Index of Major Financial Markets/387

22.3 Risk Measurement of Major Financial Markets/392

22.4 Conclusion/399

Chapter 23 Leading Indicator and Risk Transmission Path of China’s Financial Markets/401

23.1 Introduction/401

23.2 Leading Indicator Selection of Financial Markets /404

23.3 Analysis of Financial Risk Transmission Path/408

23.4 Conclusion/410

Chapter 24 Financial Risk Early Warning and Validation/412

24.1 Introduction/412

24.2 Financial Risk Early Warning Indicators and Criteria/416

24.3 Financial Risk Early Warning System in Developed Countries/419

24.4 Status of Financial Risk Warning in China/422

24.5 Construction of Financial Risk Early Warning Index and Validation/423

24.6 Conclusion/427

Part 7 Risk Control and Countermeasures of Complex Financial Systems

Chapter 25 Forecasting of Volatility of Exchange Rate of RMB Based on Multivariate Analysis/431

25.1 Introduction/431

25.2 Multivariate Volatility Models/432

25.3 Tests of Multivariate Volatility Models/437

25.4 Forecasting of Multivariate Volatility Models/438

25.5 Empirical Analysis of Forecasting for RMB Exchange Rate/439

25.6 Conclusion/444

Chapter 26 Management Method Based on Stock Index Futures Contract and Its Application/447

26.1 Introduction/447

26.2 Rollover Hedging Model with Stock Index Futures Contract/449

26.3 Optimal Rollover Hedge Strategy/454

26.4 Rollover Hedge Model and Strategy with Transaction Costs/460

26.5 Conclusion/466

Chapter 27 Portfolio Optimization Method and Its Application in Fuzzy Uncertain Environment/469

27.1 Introduction/469

27.2 Prerequisites/472

27.3 Multi-period Fuzzy Portfolio Optimization Model with Minimum Transaction Lots/474

27.4 Algorithm/480

27.5 Empirical Analysis/484

27.6 Conclusion/487

Chapter 28 Dynamic Hedging European Option Based on Stochastic Model Predictive Control/492

28.1 Introduction/492

28.2 Asset Price Change Model/494

28.3 Stochastic Model Predictive Control Based on Scenario Simulation/498

28.4 Simulation Analysis/501

28.5 Conclusion/505

Chapter 29 Countermeasures Research/508

29.1 Construction of Macro-prudential System of China’s Financial System Under the Complexity Thinking/508

29.2 Ideas of Accelerating the Construction of Systemic Risk Prevention System in Financial Markets/512

29.3 Coordinated Strategies of China’s Capital Account Liberalization,Exchange Rate Reform and the RMB Internationalization /516

29.4 Questions and Strategies of Coordination and Development of the Monetary Market and Stock Market /520

Index/527

Postscript/529

京公网安备 11010102004214号

京公网安备 11010102004214号